Testing Hedge Fund Position Sizing Alpha by AUM

In this article, we examine how hedge fund position sizing, a critical skill for creating alpha, is affected by a fund's AUM.

As we’ve previously shown, position sizing is a critical skill for a manager in creating alpha. Many factors are involved in sizing decisions, and one such factor is the AUM of the portfolio manager’s fund. A $100MM manager has more freedom in sizing decisions than a $10B manager. But does this translate into alpha, and is there a risk differential between these managers? In this post, we’ll test position-sizing alpha by manager AUM deciles to answer these questions.

Our previous research on sizing examined active sizing decisions by comparing simulated portfolio returns to an equally weighted portfolio’s return. Using that technique, we found that between 2010 and 2015, 58% of managers added alpha, the average of which was 2.8%. After looking at the industry in aggregate, we intend to dissect the data to understand if AUM size affects a manager’s ability to generate position-sizing alpha.

Position Sizing Alpha by AUM: Equal Return vs Actual Return by AUM Decile

To test for a relationship between sizing alpha and manager AUM, we decile managers in the HFU, proxying AUM with the sum of all reported market values from filings. Comparing the average return across each AUM bucket reveals a few things.

First, there’s a decrease in absolute returns with growth of assets. This is an interesting point that deserves attention, but is the topic of a separate blog post. Second, there’s a tendency for the actual portfolios to outperform their equal weight counterparts as they move up the AUM spectrum. This trend isn’t uniform across the AUM deciles, but managers with a larger asset base, on average, do generate position-sizing alpha.

This observation may seem counterintuitive, since smaller managers have more freedom to size their positions, however, there could be several reasons for this. For example, larger managers must invest in larger market caps, and those have historically done better; as a manager does well, it’s easier to raise assets and therefore grow; or perhaps the manager is making good sizing decisions. Whether it’s these factors at play or others, managers are generating performance through sizing. Managers aren’t paid to hold equally-weighted portfolios. They’re actively sizing up their names to generate further outperformance, and larger capital bases are deploying capital to their conviction names.

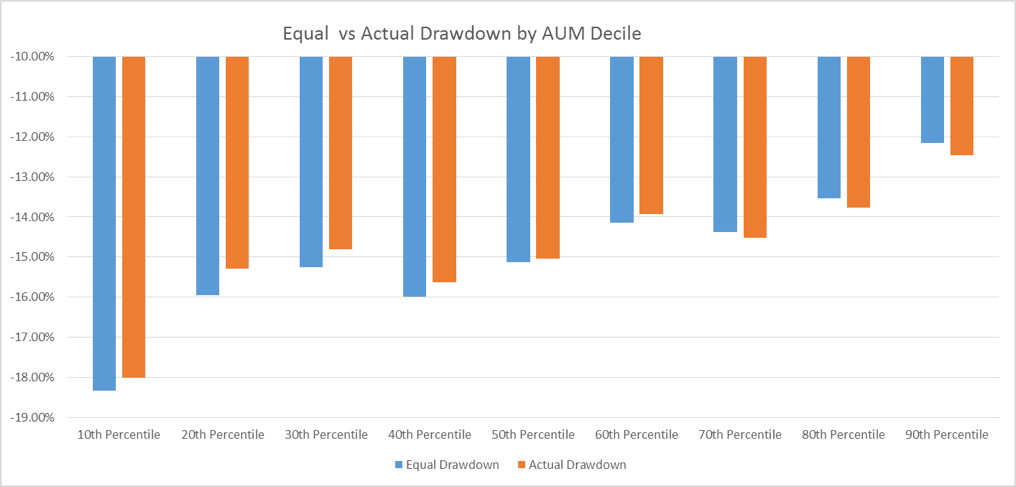

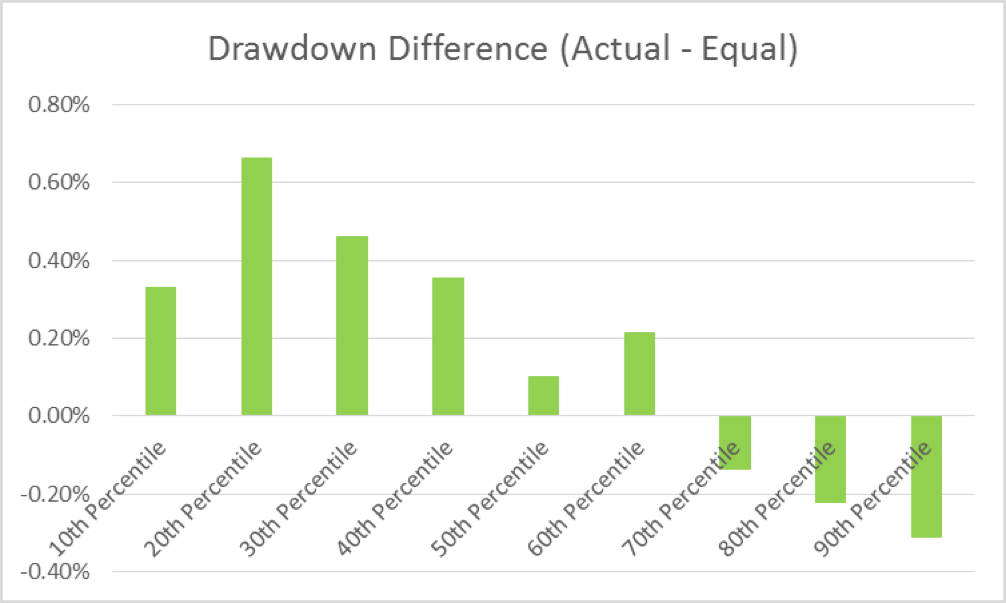

Continuing to investigate position sizing by AUM bucket, we compare the drawdown differences. Two trends emerge. First, across both actual and equally-weighted portfolios, drawdowns are smaller as AUM increases. This isn’t surprising given that larger managers tend to invest in more blue chip securities and tend to be more diversified. Second, the equally-weighted portfolio has a larger drawdown in smaller AUMs while having smaller drawdowns in the larger AUM buckets. Although drawdowns are decreasing as assets rise, the largest managers experience greater drawdowns than an equally-weighted counterpart. As we know, larger managers investing in more stable firms and with greater diversification would reduce the drawdown. That being said, larger managers may in turn have more concentrated and higher conviction trades that hurt more when they turn against them, magnifying any negative performance compared to an equally-weighted portfolio.

A similar trend appears when comparing standard deviations. Standard deviations of both portfolios decrease as the AUM increases, reflecting more stable capital, but the actual portfolio volatility increases when considered against an equally weighted portfolio. Sizing decisions on average add risk to the portfolio, manifesting itself in larger drawdowns. Investors pay managers to make active sizing decisions, and this increased volatility is part of the cost of potentially generating excess returns. Is the risk worth the reward?

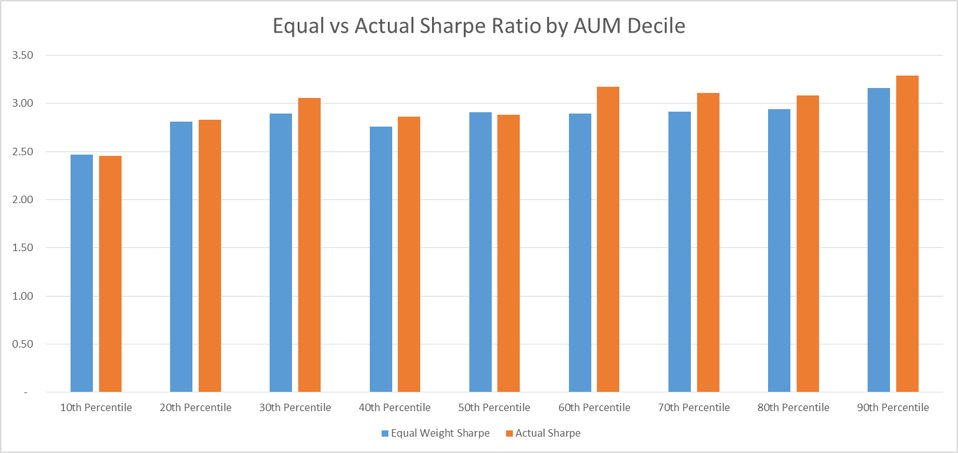

Contrasting Sharpe Ratios across AUM buckets shows that larger managers provide higher-risk adjusted returns. The sizing decisions of managers at higher AUM levels introduce volatility, but generate alpha that compensates for the additional risk.

Managers must consider sizing decisions, and what role they play in their skillset, especially as their capital base changes. These skillsets can attract or deter future and present investors. Examining the industry reveals that even though smaller managers may have greater degrees of freedom with their capital and can generate higher returns, larger managers can generate higher position-sizing alpha and do so on a risk-adjusted basis. At the end of the day, investors are paying for a manager’s skill.

Public Data:

All information used in this analysis is based on public ownership data via 13Fs and other regulatory filings. We use the Novus Hedge Fund Universe (HFU) as the basis for the analysis. The portfolio is a market-value-weighted simulation of over 1,200 manager portfolios covering $2T USD in long assets. Our data spans from 2005–2015. As managers file their positions, we simulate monthly performance in comparison to a theoretical equally weighted portfolio to identify and evaluate position-sizing decisions across the industry. Due to the nature of the filings, this is predominately focused on the long side and on equity positions. AUM refers to publicly reported assets from regulatory filings.

Technical notes:

We collected data between 2005 and 2015 and examined the annual returns of managers in comparison to an equally weighted portfolio. The active premium against this equally weighted benchmark is considered to be positive or negative alpha through position-sizing decisions. We performed this same type of comparison against standard deviation and drawdown. Finally, we compared equally weighted and actual Sharpe ratios. After deciling the data, we examined each metric regardless of year and averaged each statistic across the deciled AUM buckets.