Security Selection Alpha Declines – Small Wins & Big Losses

We'll examine the reasons why hedge fund security selection alpha has declined and summarize the implications for managers and investors.

Recent studies debating Hedge Funds’ abilities to deliver market-beating returns have reached one sobering conclusion: while a subset of managers consistently generates security selection alpha, the industry in aggregate hasn’t done well. Here we’ll explore several questions related to trends in HF alpha and investment regimes.

How has alpha from security selection changed since 2001?

Is alpha decline a result of smaller wins or larger losses?

What portfolio attributes and skill-sets are best suited for the current market environment?

Declining Contribution from Security Selection

Using our Novus Attribution Framework, we decomposed the returns from the Hedge Fund Universe—an aggregate portfolio of HF long positions based on 13F filings—into four principal components: contribution from market (i.e., market beta), sector selection, security selection, and trading acumen. Our prior research found that contributions from sector selection and trading are immaterial at the industry level. HF alpha, when examined at the aggregate level, comes almost exclusively from security selection.

Revealed below in Figure 1 are trends in alpha from security selection since 2001. Negative security selection occurred in five of the past 16 years (~30%), and three of those five instances occurred after 2014. Prior to 2008, alpha from security selection averaged ~500 bps per year. In contrast, over the past three years, equity HFs saw negative security selection alpha in the range of 200–400 bps per annum. Granted, a number of external factors contributed to the drop in alpha: increasing crowdedness, narrow market breadth, passive management/ETFs, and macro events (e.g., Brexit/Trump election) to name a few.

Diversified Wins, Concentrated Losses

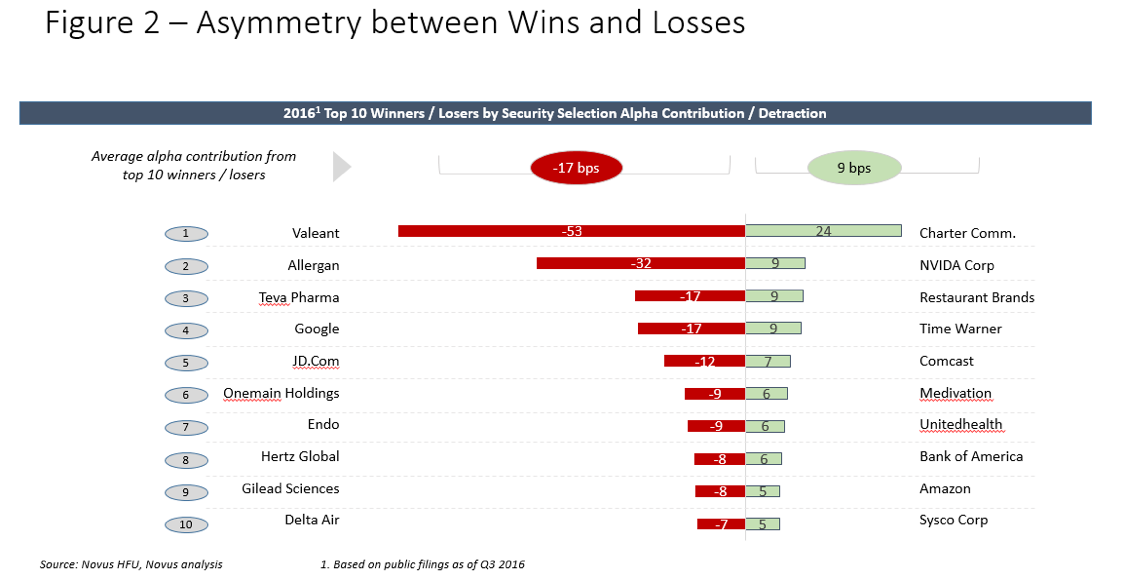

Is declining alpha a result of equity HFs producing fewer wins or suffering greater losses? Figure 2 lists the top ten alpha contributors and detractors of 2016, along with the size of the contribution. Interestingly, the average losses from top detractors nearly doubled the gains from winners (17 bps vs. 9 bps). Our current investing environment appears to foster far more diversified gains and more concentrated losses. This asymmetry suggests that the risk/reward ratio for alpha generation is poor; risk-taking in this environment, all else being equal, is more likely to result in loss (after adjusting for market exposure).

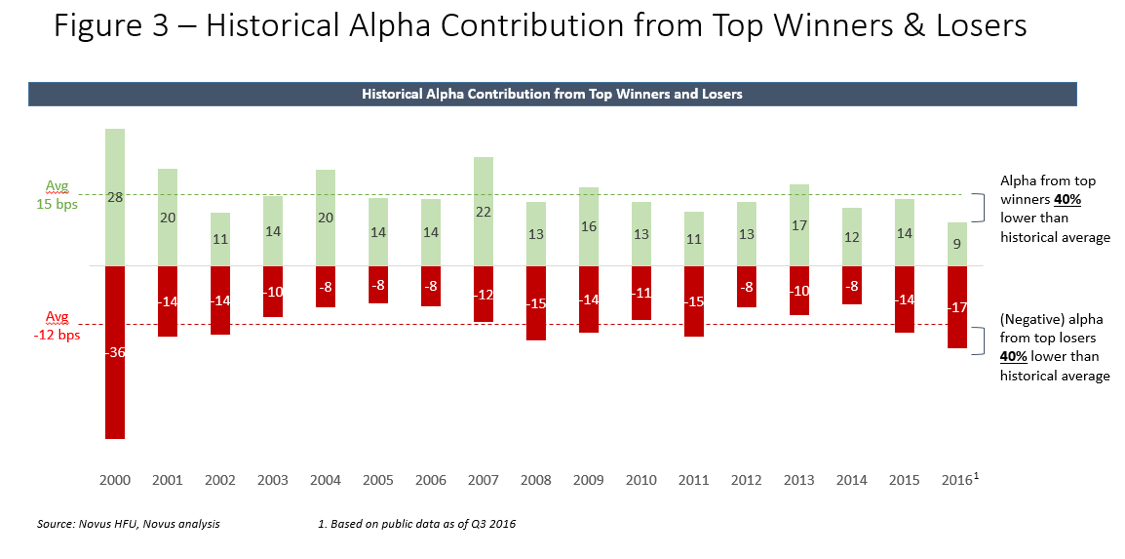

Figure 3 provides additional historical context. Depicted here are the average gains/losses from top-ten winners/losers per year since 2001. In 2016, average alpha from top-ten winners was 40% lower than historically (9bps vs. 15 bps), while the average loss among top-ten losers was 40% higher (17bps vs. 12bps)! Figure 4 further highlights the skew via win/loss ratios (i.e., average security selection from top-ten winners divided by security selection from top-ten losers for each year since 2001). The skew has never been as pronounced as it is now: in 2016, the ratio dropped to 0.5, compared to a historical average of ~1.4x.

Another observation is that security selection alpha appears to be cyclical. As exhibited in Figure 2, since 2001, security selection from winners had a peak-to-peak cycle of three to six years on average. 2016 was the third year since the last peak. Security selection from losers had a trough-to-trough cycle of three to six years as well. 2016 was the fifth year since the last trough. If the recent past is any indication, 2017 could be the beginning of a recovery. Based on this past month’s cautiously optimistic outlook reports regarding trends in earnings and expectations for earnings growth, likelihood of rise in rates, and potential tax and regulatory reforms, this seems quite possible.

Implications for Managers and Allocators

How might win/loss size impact the decision-making of HF managers and allocators? To address this question, we tested the correlation between certain trade characteristics and alpha contribution size. Specifically, we asked if top alpha contributors/detractors tend to be consensus, conviction, concentrated, or crowded trades. Novus constructs four indices based on characteristics of long positions held by HFs, rebalanced monthly. Through these indices, we monitor the changing opportunity set with respect to trade characteristics. Note that some securities may exist in more than one index. On average, we see ~30–50% overlap between the Consensus and Conviction Index, and ~10–30% overlap between the Crowded and Concentration Index:

Conviction Index – List of twenty stocks with the highest number of HFs invested with conviction (5% of an HF portfolio).

Concentration Index – List of twenty stocks with the highest percentage of shares held by HFs.

Consensus Index – List of twenty stocks with the highest HF participation in terms of number of managers (i.e., most frequently traded names).

Crowded Index – List of twenty crowded stocks per Novus Crowding score.

Figure 5 shows the historical correlation between the alpha contribution size of top winners/losers with 4 Novus indices (from 2004 to 2016). Interestingly, we find the drivers for positive and negative alpha to be very distinct: positive alpha (by top winners) is strongly correlated with the Conviction Index (86% correlation). Negative alpha (by top losers), on the other hand, is correlated with the Concentration Index (62% correlation).

The Conviction Index essentially tracks the stocks that HFs invest in with the highest conviction—i.e., the “chunkiest” positions in their portfolios. In an investing environment where winner alpha is broadly lower, the key word for managers and allocators should be “diversify” (and “concentrate” if winner alpha is high). Fundamental managers might want to consider, for example, increasing the number of positions/themes in the portfolio where possible. Allocators should perhaps lean into diversified strategies, as well as larger HFs, who (on average) run more diversified portfolios than smaller peers. Regarding skill-sets, we expect batting averages to rise in importance relative to win/loss ratios (i.e., consistency more important than slugging). Portfolio management skills like position sizing (Are you getting paid for leaning into your convictions?), exposure management (Are you adding value by swinging your net and gross exposure?), and turnover management (Are you turning over your portfolio too little or too often?) also matter more. Overall, both HFs and allocators need to assess and quantify broader skill-sets in an investing environment with average lower alpha wins.

The size of negative alpha (from top losers), on the other hand, tends to correlate to the Concentration Index. This index tracks a list of twenty stocks with the highest percentage of shares held by HFs. The most concentrated stocks, by this definition, also tend to be the most illiquid. Our analysis shows that these stocks often drove the biggest losses. Therefore, when overall environment is characterized by concentrated losses, liquidity is paramount. Managers must focus on liquidity management as a top priority. There’s usually a low level of illiquidity premium in these environments, as shown in our prior research. This also means that it’s not only important to concentrate on security fundamentals, but to also have a “market view” taking into account investors in the same securities.

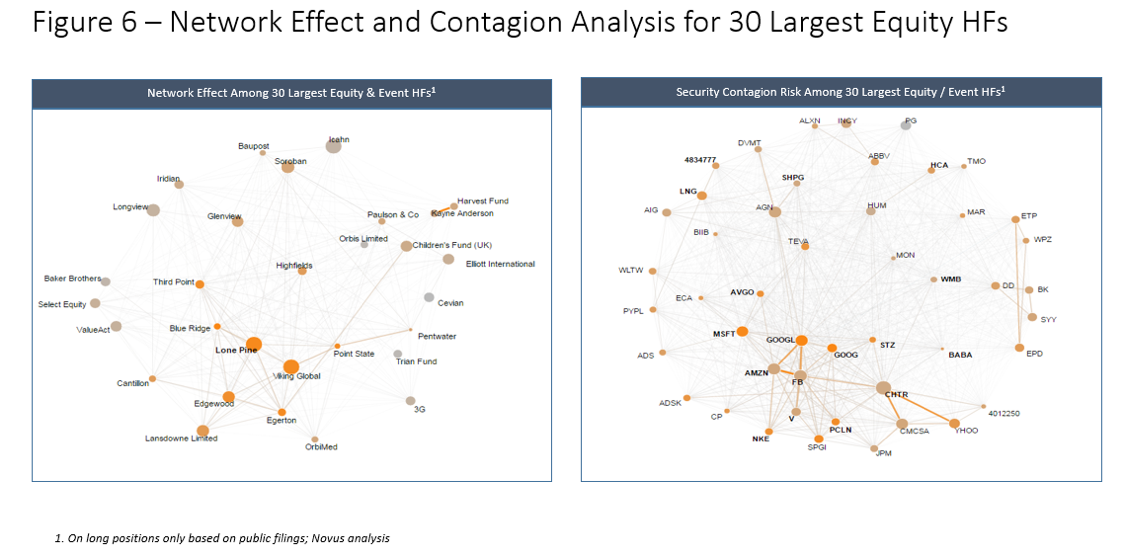

Our Novus Holdings report publishes the number of HF investors by position, broken out by number of buys/sells/holds/entrants/exits on a quarterly basis. HF allocators should pay special attention to allocations in less liquid strategies where HFs comprise the majority of total market. They might also want to increase surveillance on the amount of position overlap among their managers. More sophisticated HFs and allocators raise the bar by factoring in potential security contagion risks, or likelihood of co-occurrence among securities in a de-risking event. To demonstrate this, Figure 6 displays how an HF or HF allocator may analyze network effect and contagion risks among the thirty largest HFs using the Novus platform.

The chart on the left presents the network/overlap among the thirty largest Equity and Event managers (based on size of long portfolios). The size of the node indicates the manager’s AUM size. The links between nodes represent the strength of the relationship, with highly overlapping portfolios closer together. A shorter, thicker line represents a stronger overlap between nodes. A HF with more links is likely to be more central to the network, where a manager on the periphery tends to be more unique. In our example, Lone Pine and Viking Global stand out as two managers with the greatest overlap. (This may not necessarily be a negative indicator—as one manager said to us, “You know you’re good if you’re being copied.”)

The chart to the right takes the network effect this one step further, displaying co-occurrence activities between securities held by managers in this group. Stronger links imply that two securities will more likely be found together in size among the portfolios in the group. If a security is more central to the network, it has more pair-wise occurrences and thus may be more susceptible to contagion, depending on liquidity. In our example, Google, Amazon, and Facebook have a strong likelihood of moving together; therefore, if one of these securities’ outlooks changes, the other two are likely to move as well, even though the fundamentals haven’t changed.

In summary, generating alpha in the current environment requires a much broader set of skills than bottom up research.

Since wins are diversified, HFs and allocators must assess/quantify a myriad of portfolio management skills to ensure optimal and sufficient diversification; and since losses are concentrated, HFs/allocators should also focus on liquidity risks by factoring crowdedness, overlap, and contagion into their decision-making.

We would like to give our special thanks to John K. Atsalis from Tufts University for his insights and guidance on this piece.