2018: Active Management Back in Favor

Major investment firms have published their year-end market outlooks. Here is what we learned about active management and its 2018 prospects.

At the end of 2017, major investment firms published their “house views” on the 2018 markets. We reviewed over a dozen of these market outlooks to understand the current consensus on major investment themes. In addition to commentary on synchronized global growth and elevated equity valuations, nearly every firm viewed active management positively for the next twelve months (although they may also have a vested interest behind that view). Three trends are expected to aid active managers’ relative performance in the coming year: reduction of supportive monetary policy, increased volatility, and widening dispersion. Let’s discuss how these external conditions could benefit active management.

Volatility Returns

As this is being written, the volatility prediction is playing out. The CBOE VIX rose above 40 intra-day on February 6th, and CBOE SKEW rose to nearly 150 the following week. SKEW is an indicator of the market’s tail risk, calculated from the prices of S&P 500 out-of-the-money options (low strike puts).

Less Monetary Support → Lower Equity Correlations

The consensus is that less supportive monetary policy will lead to greater price sensitivity from individual company fundamentals (idiosyncratic risk), which in turn should lower pair-wise correlations.

UBS —“Reduced central bank support should make stocks more responsive to idiosyncratic factors. This could aid active managers, who have previously underperformed as central bank policy support helped all stocks move up together.”

Wells Fargo —“Unprecedented quantitative easing after the financial crisis caused a distortion in prices, a suppression of volatility, and a reduced emphasis on corporate fundamentals. Passive investing thrived in such an environment. As the era of quantitative monetary stimulus slowly winds down, we continue to forecast an improved environment for active management.”

Lazard —“Our strong belief is that security selection will be critical to generating returns in the years ahead, as global growth normalizes and the ‘easy money’ of the market rallies in recent years is harder to come by.”

Last October, the Federal Reserve started the balance-sheet normalization program:

and it is continuing with interest rate increases:

And as we see below, correlations are already falling.

While lower correlations are related to active performance, our research team found that higher dispersion is even more significant (“Is Poor Performance Always Tied to Manager Ability?”). Vanguard took this stance a step further in their research piece “Dispersion! Not correlation!”

Dispersion: Sector, Style, & Region

From 2013 to 2016, sector dispersion was quite low as the broad market expanded with monetary stimulus. Cyclical and growth sectors had similar returns (apart from Energy), as did non-cyclical sectors.

As 2018 progresses, the consensus is that sector dispersion will rise. (Stock-pickers rejoice!)

HSBC —“Country and sector correlations also continue to weaken, and the increased dispersion within equity markets creates a more conducive environment for managers to identify winners and losers. As a result, we believe there is strong potential for alpha through security selection on both long and short books in 2018.”

UBP —“Style and sector selection should also be helpful in the environment we see ahead.”

Franklin Templeton —“High levels of policy uncertainty and regional divergences will cause higher dispersion across and within asset classes, in our opinion, which increases the attractiveness of active management in both asset allocation and at the security-selection level.”

Wells Fargo —“We have strong conviction that long/short equity strategies should benefit from favorable conditions in 2018. We expect greater fundamental dispersion among sectors, industries, and geographies in the year ahead, as well as greater dispersion among the prices and returns on equities. Such an environment tends to lead to lower correlations among equity assets and more opportunities to add value through both long and short investments. We expect these trends to strengthen and become even more favorable for active managers as the economic cycle matures and the winners become more easily discernible from the losers.”

Wellington Management —“We expect disruptive forces to continue creating individual winners and losers within many sectors, a trend that has provided a more attractive environment for active management.”

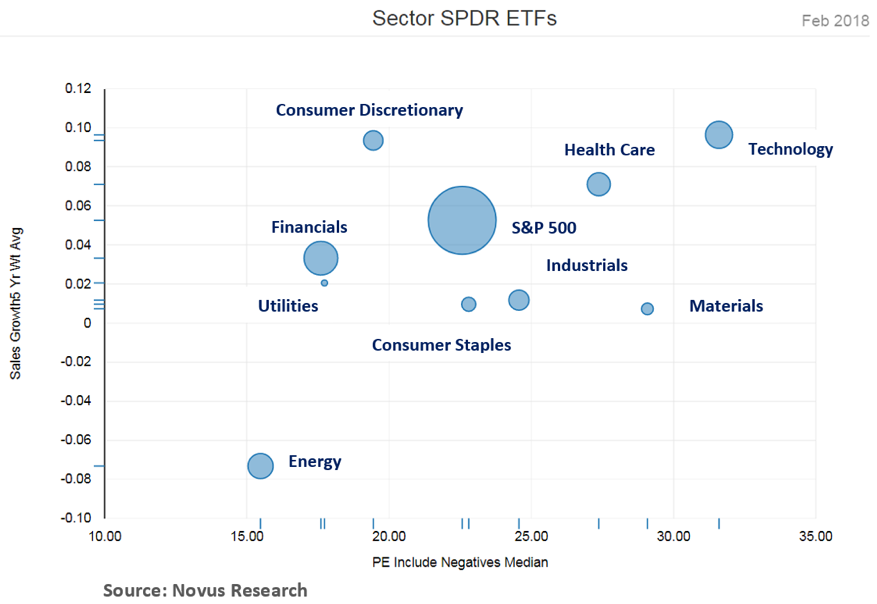

Dispersion will likely rise with sectors scattered across the valuation and growth spectrum:

Style dispersion is also creating opportunities for active managers. 2017 ended with the outperformance of growth vs. value. Moving into 2018, the market is pricing in Federal tax changes, which is a near-term catalyst for higher sector dispersion.

Goldman Sachs —“Expect more sector dispersion, potentially benefiting domestic [capex-intensive companies] and high-tax companies (i.e. value and small- and mid-cap stocks) vs. globally exposed, [high interest expense], and lower tax sectors (including Tech and Healthcare). However, the latter group could see some offsetting benefits from repatriated cash, which could be used to fund M&A and buybacks.”

Finally, active managers with experience investing abroad benefit from dispersion across certain countries and regions. A great example of this is the dispersion between global technology stocks:

Takeaway

Reduction of supportive monetary policy, return of volatility, and increased dispersion across sectors, regions, and styles should bode well for active managers in 2018.